Rethink Risk with Strategies Beyond Traditional Insurance

What Are Alternative Risk Strategies in Insurance?

Alternative risk strategies are methods of financing risk outside the traditional insurance market. Instead of fully transferring risk to an insurer, businesses retain or share a portion of it—often gaining greater cost control and long-term financial advantages.

Common alternative risk financing solutions include:

- Captive Insurance Programs (owning or participating in your own insurance company)

- Self-Insurance Strategies

- Risk Retention Structures

- Large Deductible Plans

- Alternative Risk Transfer Models

For companies facing rising premiums or unpredictable renewal cycles, these approaches can offer stability and strategic control.

Why Businesses Consider Alternative Risk Strategies

Sophisticated organizations often explore non-traditional insurance when they feel trapped by market volatility or escalating costs. Benefits can include:

Cost Efficiency Over Time

Retaining predictable risk can reduce long-term premium expense and limit exposure to pricing cycles.

Greater Control

More influence over claims handling, risk management decisions, and underwriting structure.

Cash Flow Advantages

Retained funds may be invested or reserved strategically rather than paid entirely to insurers.

Potential Profit Participation

If losses are lower than expected, the financial upside stays with your organization—not the carrier.

Customization

Coverage structures designed around your actual risk profile, not generic industry averages.

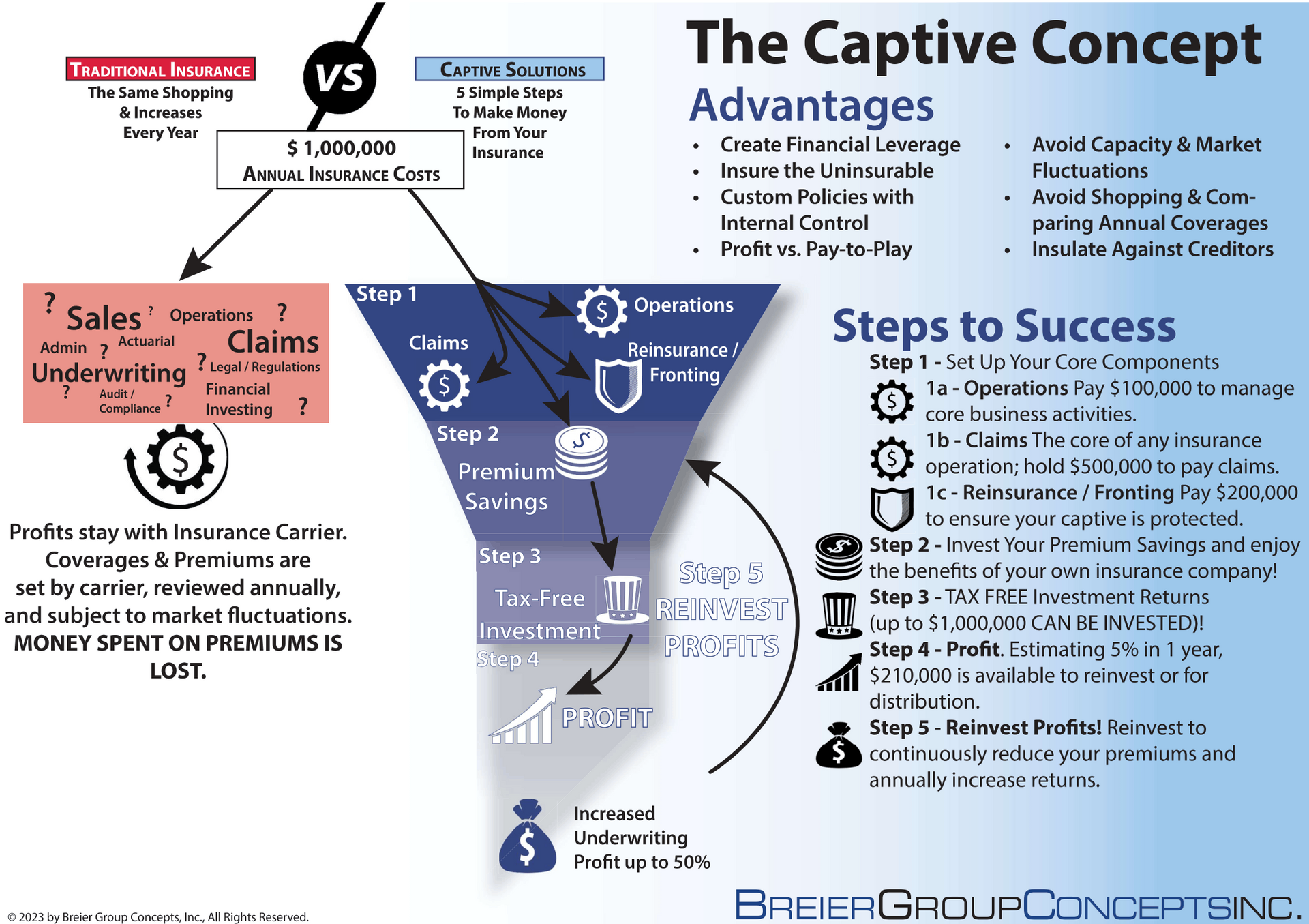

Captive Insurance Programs Explained

A captive insurance program allows your company (or a group of companies) to form or participate in its own licensed insurance entity. Instead of paying premiums solely to a commercial carrier, you retain underwriting profit and exercise greater oversight over claims and reserves.

Captives can be structured in multiple ways—single-parent, group, or cell captives—depending on your size and risk appetite. Breier Group Concepts conducts feasibility analyses to determine if a captive insurance strategy aligns with your financial objectives.

Large Deductible and Hybrid Self-Insurance Strategies

Not every company is ready for a full captive. Hybrid models may include:

Large deductible programs with stop-loss protection

Partial self-insurance paired with traditional coverage

Layered risk retention models

These structures allow you to reduce premiums while still maintaining protection against catastrophic losses.

Who Is a Good Candidate?

Alternative risk strategies may make sense if:

Legal defense costs for infringement claims

Settlement payments or court judgments

Expert witness and litigation expenses

Enforcement coverage (in some policies) if you must pursue an infringer

Coverage for patent, trademark, and copyright disputes

Mid-sized and larger organizations often benefit most, but each case requires careful analysis.

How Breier Group Guides the Process

Alternative risk financing requires thoughtful planning. Our team evaluates your loss history, financial strength, operational risk, and long-term objectives before making any recommendation.

If a captive or self-insurance strategy is appropriate, we coordinate with actuaries, captive managers, and legal advisors to design and implement the structure properly. If it's not the right fit, we'll say so and recommend a more suitable solution. Our goal is improved outcomes—not complexity for its own sake.

Take Back Control of Your Insurance Strategy

If rising premiums feel unpredictable or unsustainable, it may be time to explore alternative risk transfer options. With the right structure, your insurance program can become a strategic financial tool—not just an annual expense.

Common Questions About Alternative Risk Strategies

What are alternative risk strategies in insurance?

They are methods that allow businesses to retain or finance risk outside traditional commercial insurance, including captives, self-insurance, and large deductible programs.

How does captive insurance work for a mid-sized business?

A captive allows a company to insure its own risks through a controlled insurance entity, potentially retaining underwriting profit while gaining more control over claims and reserves.

Can alternative risk strategies reduce insurance costs?

For companies with stable loss histories and strong risk controls, these strategies can stabilize and potentially reduce long-term costs.

Are alternative risk programs safe to implement?

They require proper structuring and financial analysis. When designed correctly, they balance retained risk with protections such as stop-loss coverage.

How do I know if my company qualifies?

The first step is a feasibility assessment. We review financials, claims history, and operational risk to determine suitability.

Explore a Smarter Way to Manage Risk

Insurance doesn't have to be limited to traditional policies. Breier Group Concepts helps businesses across the New York Tri-State Area and beyond evaluate alternative risk financing solutions that align with long-term financial goals and operational strategy.